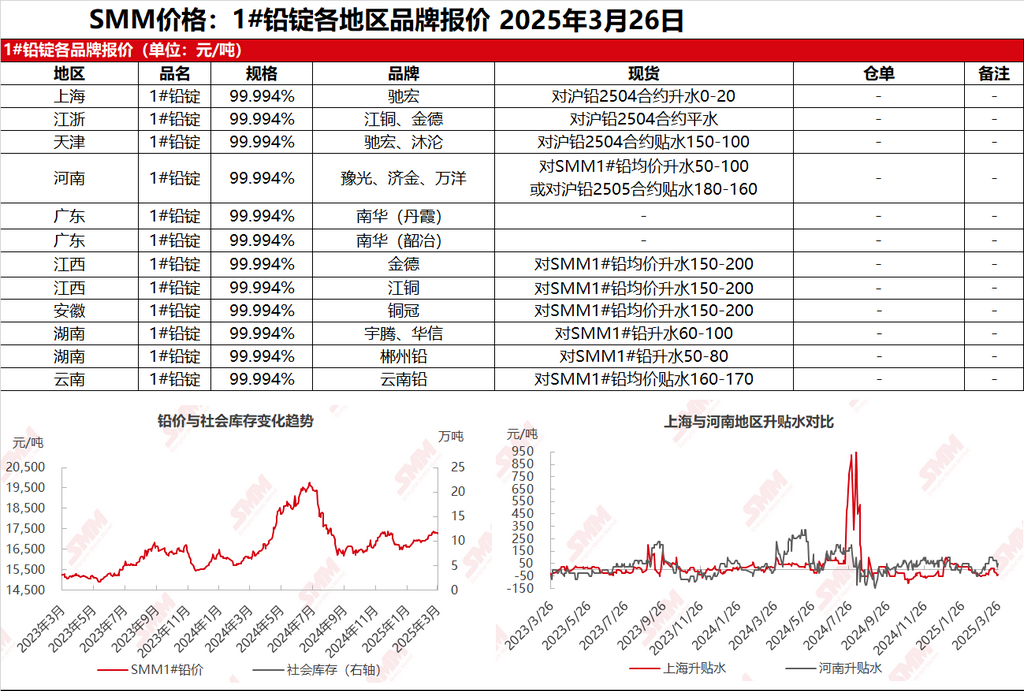

SMM March 26 news: In the Shanghai market, Chihong lead was quoted at 17,515-17,550 yuan/mt, with premiums of 0-20 yuan/mt against the SHFE 2504 lead contract. In the Jiangsu-Zhejiang region, JCC and Jinde lead were quoted at 17,515-17,530 yuan/mt, at parity against the SHFE 2504 lead contract. SHFE lead fluctuated upward, with suppliers quoting prices accordingly. Due to limited circulating cargoes, there were small premium quotations. In the primary lead smelter's self-picked up cargoes, supply differences emerged between the north and south. Supply in the southern region was relatively ample, coupled with secondary refined lead being sold at large discounts (discounts of 150-100 yuan/mt ex-factory against the SMM 1# lead average price). Downstream enterprises selectively procured, leading to subdued spot transactions in the southern region.

Other markets: Today, the SMM 1# lead price increased by 25 yuan/mt compared to the previous trading day. In Henan, smelters had limited inventory, mainly shipping under long-term contracts. Suppliers quoted discounts of 160-180 yuan/mt against the SHFE 2505 lead contract. In Hunan, suppliers quoted premiums of 50-100 yuan/mt against the SMM 1# lead price. In Yunnan, some small plants resumed production, with spot orders quoted at discounts of 160-170 yuan/mt against the SMM 1# lead average price. During the month-end period, new long-term contracts for lead ingots began to be delivered. Downstream enterprises generally purchased as needed, with high lead prices leading to a wait-and-see attitude in the market, resulting in subdued transactions.